Five thousand dollars. A hundred and fifty thousand. Three hundred and fifty thousand.

Those are not three companies' valuations. They are the same offer - a startup cloud credit package - quoted by three different providers to a founder asking the same question on the same day. The spread is not a rounding error. It is the entire comparison most founders never run, because they assume the three big clouds are close enough on price that the choice comes down to which one their first hire already knows.

It doesn't. The compute is close to identical. The subsidy is not. And the subsidy is the first real negotiation a founder has with a cloud vendor - usually the one they're least prepared for, because nobody told them it was a negotiation at all.

Why This Decision Matters Before You've Spent a Dollar

Founders tend to treat the cloud-provider choice as a technical decision to be delegated - pick whatever the first engineer prefers, move on to the product. That instinct is understandable and almost always wrong, for a reason that has nothing to do with engineering preference: most companies are already losing money on cloud before they even notice.

Flexera's 2025 State of the Cloud Report - based on a survey of more than 750 technical and executive leaders - found that organizations waste an average of 27% of what they spend on cloud infrastructure, on unused or over-provisioned resources nobody remembered to turn off. Eighty-four percent said managing cloud spend is their top cloud challenge, full stop - ahead of security, ahead of skills gaps, ahead of everything else on the list.

That number is the backdrop against which every credit offer should be read. A founder who picks a provider purely on the size of the signing bonus, then runs the same undisciplined spend pattern as everyone else, isn't capturing the subsidy - they're just delaying the moment they discover the waste. The provider comparison and the cost-discipline problem are two different fights. This article is about winning the first one. The practical mechanics of winning the second are covered in depth in Cloud Cost Reduction Without Slowing Engineering - the playbook for what to do once you're in the room with an account manager and need to make every dollar of commitment count.

Who Is Actually Competing for You

Start with where the three providers actually stand, because market position determines how hard each one will fight for your business - and "fight" here means money and terms, not marketing copy.

Synergy Research Group's Q1 2026 figures put AWS at 28% of the global cloud infrastructure market, Microsoft Azure at 21%, and Google Cloud at 14% - with the three together controlling roughly two-thirds of a market now running at an annualized rate north of $500 billion.

Read on its own, that chart looks like a story about AWS's dominance. Put a second number next to it, and it becomes a story about who needs you more.

A provider sitting at 14% share with the fastest growth of the three has a structurally different reason to subsidize you than a provider that already owns more than a quarter of the market and can afford to let founders come to it. When you read a credit offer, read it as a signal of how badly the vendor needs your growth story - because in the early relationship, that need is the only leverage a pre-revenue founder actually holds.

The Credit Stack: What's Actually on the Table, and Who Gets Frozen Out

Here is what each provider is offering as of mid-2026 - and, more importantly, who actually qualifies for the headline number versus the asterisk underneath it.

AWS Activate tops out around $100,000-$200,000 in standard credits, and AWS separately committed $230 million specifically to generative AI startups in 2024 through its Generative AI Accelerator - additional credits plus mentorship and go-to-market support layered on top of the base program.

Google Cloud for Startups, on its AI track, can stack to roughly $350,000 over two years - a 100% match up to $250,000 in year one, then 20% up to $100,000 in year two - but that ceiling generally requires an accelerator or VC partnership, not a solo application from a garage.

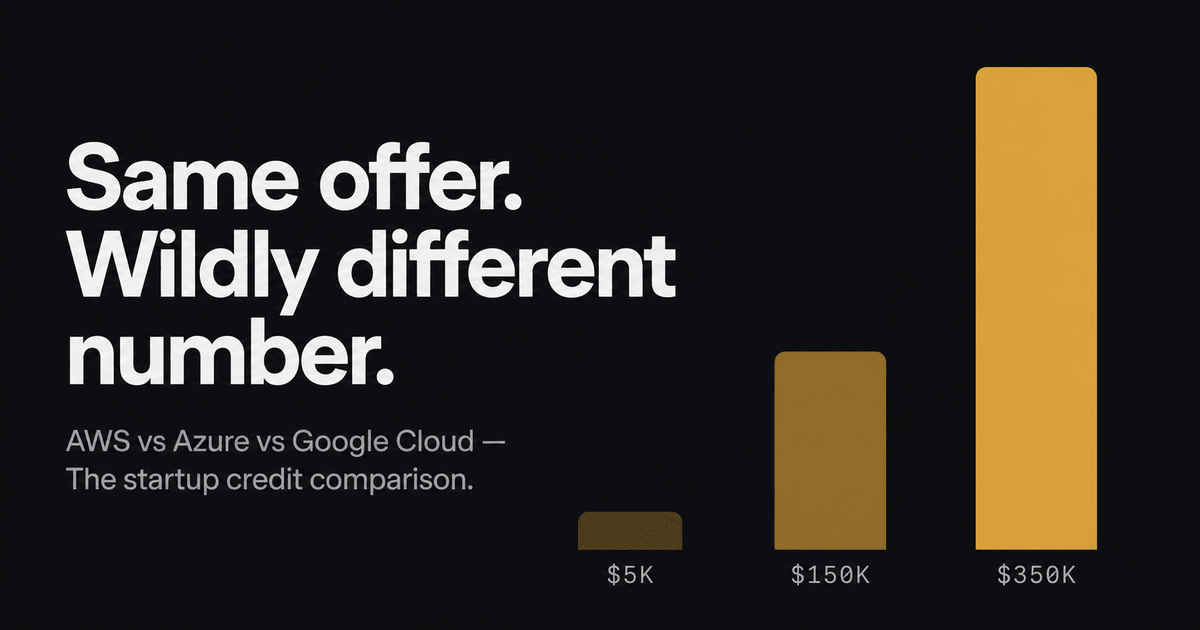

Microsoft for Startups Founders Hub is the one to read most carefully, because the terms moved under founders' feet. As of its July 2025 policy change, the marquee $150,000 Azure credit tier requires investor-network affiliation. A bootstrapped founder with no institutional backing is now routed to a roughly $5,000 baseline.

That gap is the whole game, and it isn't unique to Microsoft - it's simply the most documented version of a pattern that runs through every provider's startup program. The biggest number on a homepage is not the number on offer to your company. The first hour of comparison-shopping a cloud vendor should go to finding the eligibility gate, not admiring the ceiling - because the gate determines whether the rest of the comparison even applies to you. A founder who applies to three programs assuming the headline figures are real, and gets routed to the baseline tier on all three, has just spent a week of runway discovering that the "comparison" they thought they were running was a comparison of marketing pages.

The Quiet Difference: What You Get Besides Money

Credits are now table stakes - every serious provider matches roughly the same range, gated in roughly the same way. What's actually scarce is something that doesn't show up on a pricing page at all: a named person, at a real company, willing to attach their name to a claim about how the support showed up when it actually mattered.

Microsoft is the provider that publishes those names. Paroma Varma, co-founder and head of research at Snorkel AI, is quoted directly on Microsoft's founder-stories page crediting "the expert technical guidance from Microsoft for Startups" with accelerating her company's product development - alongside several other named founders describing the program in similarly direct, attributable terms, including one who called it "instrumental to the success of" their company.

AWS and Google Cloud's public startup materials lean almost entirely on aggregate statistics - dollar totals, startup counts, program scale, the kind of numbers that are true and also tell you nothing about Tuesday afternoon when your database falls over. That's not necessarily a quality gap; it may simply be a publishing choice, a different theory of what convinces a founder to apply. But it is a real, checkable asymmetry, and asymmetries are where the actual signal lives. One vendor has decided that a founder's name on a quote is worth more to its growth story than another aggregate figure. The other two have decided the opposite.

Worth stating plainly, because the skeptical reading is the correct one to hold alongside the generous one: these are vendor-published testimonials, not independent reporting, and should be weighed as exactly that - marketing with a name attached, not journalism. But the fact that only one of the three providers chooses to lead with named voices instead of aggregate numbers is, on its own, the finding worth carrying into your evaluation. It tells you which vendor is building its pitch around the relationship, and which two are building theirs around the scale.

When the Subsidy Ends

Every comparison of cloud providers that stops at the signing bonus has skipped the part that actually determines whether the choice was a good one: what happens when the free money runs out, and how each vendor behaves once you're no longer being courted.

Most startup credit programs run on a 12-to-24 month window. The providers offering the longer runway - Google's two-year AI track against the more common single-year cliff elsewhere - are not simply being generous. They are buying themselves more time to get your architecture wired into their specific managed services before the bill becomes real. Every month you spend building on a provider's proprietary tooling while the meter is subsidized is a month of switching cost compounding quietly in the background, invisible until the day you actually try to leave.

The pattern that follows credit expiration is consistent enough that the industry now has a name for it: the "credit cliff" - the jump from a near-zero monthly bill to a five-figure one inside a single billing cycle, landing on a company that built its architecture during the free phase without ever having to think about cost. Combine that cliff with Flexera's finding that the average organization is already wasting 27% of whatever it spends, and the arithmetic gets uncomfortable fast: the same instinct that let the waste accumulate during the subsidized phase is what turns the cliff into a crisis instead of a line item.

What each provider does next diverges sharply, and this is where the comparison earns its keep:

AWS moves you toward Enterprise Discount Programs - multi-year committed-spend contracts with volume-based tiering. The relationship becomes a negotiation over how much of your future usage you're willing to pre-commit, in exchange for a discount on usage you haven't generated yet.

Azure leans on Enterprise Agreements and co-sell motion. Your cloud discount increasingly becomes a function of how much of the broader Microsoft ecosystem - Office, Dynamics, GitHub, the Copilot stack - you're willing to adopt alongside it. The "cloud deal" quietly becomes a "Microsoft relationship," and the second is a much bigger commitment than the first.

Google Cloud's committed-use and sustained-use discounts are comparatively more granular and workload-specific. That gives a technically sophisticated team more room to negotiate on its own terms - and gives a non-technical founder considerably more room to leave money on the table without ever knowing it was there.

None of these models is predatory. All three are rational. But "rational for the vendor" and "good for a three-person company that just lost its subsidy" are not the same sentence, and the gap between them is exactly where the next stage of the relationship gets decided - usually by whichever side did more homework before the conversation started.

The Comparison Founders Should Actually Run

Strip away the marketing pages and the three providers resolve into three distinct bets, not three flavors of the same thing:

AWS is the safest default, the deepest ecosystem, and the hardest provider to extract a generous early deal from - because at 28% share and a $230M generative-AI commitment that still represents a rounding error against its scale, it doesn't need any single founder's growth story the way the other two do. You are choosing maturity and breadth over negotiating leverage.

Google Cloud is the most aggressive on AI-specific credits precisely because it is fighting from third place with the fastest growth rate of the three - a vendor in that position has to compete on terms, not just infrastructure quality. You are choosing a larger initial subsidy and a faster-moving AI stack, in exchange for betting on the smallest ecosystem of the three.

Azure is playing the longest commercial game of the three. It will hand you real money - but increasingly only if you are willing to become part of a larger Microsoft relationship that extends well past your cloud bill, into the tools your whole company runs on. You are choosing distribution and enterprise credibility over independence.

None of these is a wrong answer for every company. What's wrong is treating the decision as a compute-pricing exercise when the real spread between the three offers is measured in tens of thousands of dollars of free runway, multi-year switching costs, and years of negotiating leverage that most founders never discover they had - because they never asked the question that would have surfaced it.

The provider offering you the largest credit is not doing you a favor. It is making the opening move in a negotiation it expects to win over the following five years. Read the terms before you take the money - because the terms, not the dollar figure on the homepage, are the actual offer on the table.

Sources

- Synergy Research Group (2026), "Cloud Market Share Trends - Big Three Together Hold 63% While Oracle and the Neoclouds Inch Higher": srgresearch.com

- Synergy Research Group / Data Center Dynamics (2026), "Cloud Spending Hits $129bn in Q1 2026, Ninth Consecutive Quarter of Growth": datacenterdynamics.com

- AWS (2024-2026), "AWS Activate Credits" and Generative AI Accelerator program details: aws.amazon.com/startups/credits

- Google Cloud, "Google for Startups Cloud Program" eligibility and AI-track terms: cloud.google.com/startup/apply

- Microsoft, "Microsoft for Startups Founder Stories" (Paroma Varma / Snorkel AI testimonial and program eligibility terms): microsoft.com/en/startups/founder-stories

- Flexera (2025), "2025 State of the Cloud Report" - cloud waste and spend-management findings from a survey of 750+ technical and executive leaders: flexera.com

Working through the challenges in this post? I help engineering leaders and CTOs navigate complex technical decisions and scale high-performing teams. Schedule a consultation →